Yea, I said it! Dave Ramsey is WRONG. Wrong. Wrong.

While Dave does teach some tactics that lead to better spending habits, most of the other stuff he teaches is going to make a lot of people miss out on wealth building. I know Dave is a lot of people’s favorite financial guru, so before you close out your browser… Hear me out…

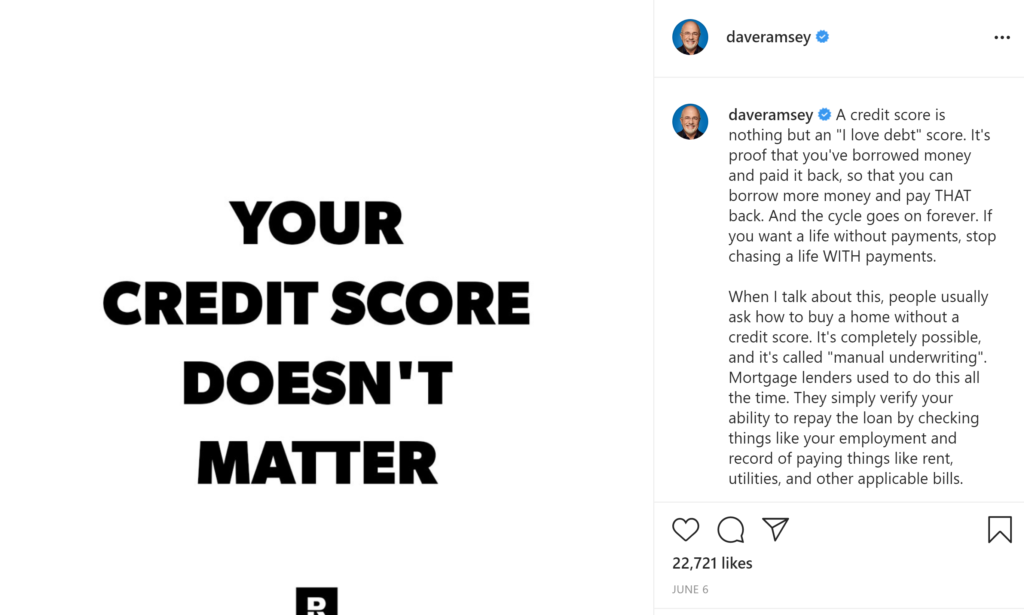

Dave’s Bad Advice #1: You Should NEVER Use Credit Cards

Dave posted this BS on his Instagram account recently and it’s so infuriating because instead of talking about using credit cards properly he’s saying that you should not use them at all and that your credit score does not matter.

He claims that if you use credit cards you are spending above your means. That is not always the case. Now, there was a time when I was that person- spending money I didn’t have and paying tons of interest on purchases, but now my credit cards PAY ME.

Here’s how to get your credit card company to pay you:

Use credit cards to purchase items that you can afford –> accrue credit cards points on those purchases —> pay the balance on time each billing cycle before interest accrues –> use credit card reward points to get cash back, book travel, or buy whatever you want. Now you’re building excellent credit AND getting paid to do it.

Dave’s Bad Advice #2: You Shouldn’t Invest Until You Are Completely Debt Free

For years Dave Ramsey has been telling people that they should not invest until they are completely debt free. No student loans, no car loans, no mortgage, no credit card debt, nothing. He says that ALL of that should be paid off before you start letting your money make money. Now I can agree with eliminating credit card debt, and having an emergency fund before investing…but having NO debt at all before you can invest…that is terrible advice.

For many people, that would mean waiting yearssssss while they work towards paying off debt before investing.

In those years spent waiting to be debt free, you are missing out on the opportunity to make money through investing (which could help you pay off debt faster!)

You shouldn’t have to decide between paying down debt or investing. You can do BOTH.

Have you guys met Teri Ijeoma? (Or seen her around the internet?). She is a stock trader and she was able to pay off $71,000 in debt with the money she made from day trading stocks this year alone!

If Teri would have held off investing until after her student loans were paid off, she would have to rely solely on her earned income from her job, to slowly pay the loans off over time. Instead, she was able to quit her job and travel full time while day trading covers her living expenses and pays off her debt.

She teaches people how she makes over $1,000 a day right from her phone from wherever she is in the world. Here’s the kicker- she only spends a couple of hours a day trading and can still make $1,000 or more…PER DAY! Just imagine the debt you could pay off with that extra stream of income. (My husband and I enrolled in Teri’s course and have had many $1,000+ days. The course is excellent.)

Or take a look at this video from James and Tanesia where they talk about how they started buying rental properties with the sole purpose of having the rental income pay off their student loan debt. That’s how you do it! Buy assets to pay your debts instead of relying on your earned income, which could take YEARS. (You can find this power couple here on IG.)

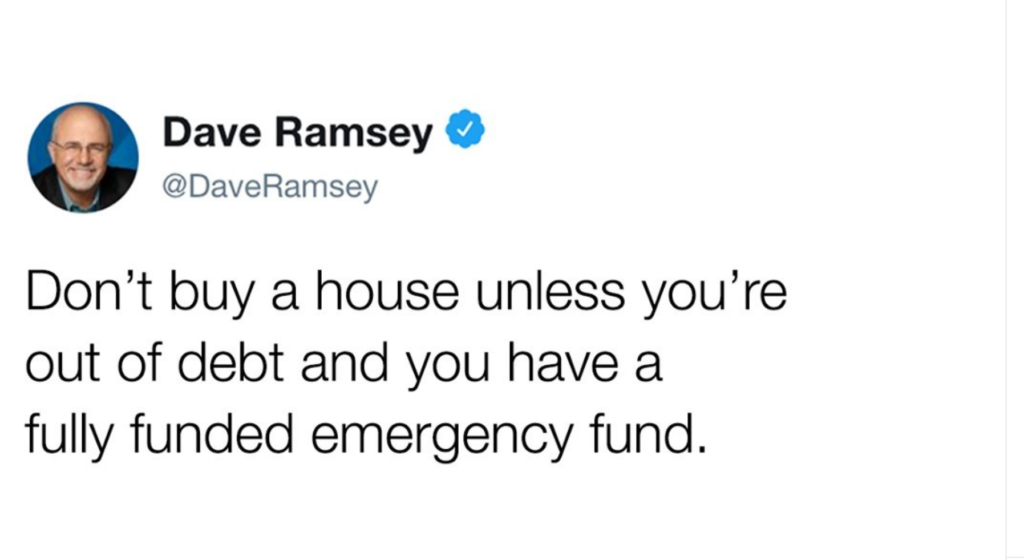

Dave’s Bad Advice #3: You Shouldn’t Buy a Home Until You Can Afford to Buy it CASH

Owning real estate is one of the cornerstones of wealth building. So imagine having to wait until you could afford to buy a house cash before you could capitalize on this method of building wealth. It is INSANE. In most markets these days, the average house costs upwards of $200,000 (and if you’re in an expensive market like LA, DC, or NY, you’d be lucky if you found anything under $400,000 right now). So Dave is saying that you should not buy a house until you are completely debt free AND until you can afford to pay for the house in cash. Just think about how long that would take the average person to achieve. You’re supposed to pay off your 6 figure student loan debt, pay your every day bills AND save 6 figures to buy a house cash? HOW SWAY?!

Don’t get me wrong, I am not saying that this is impossible for everyone- there are some people that have high salaries and/or side hustles that may make this easy for them to achieve…but to speak in absolutes saying that everyone should do this just isn’t fair, and it’s downright irresponsible.

To be honest, even if you had $400k cash in the bank, I’d still say consider getting a mortgage because LEVERAGE is the tool of the wealthy. If you had $400k in the bank, why spend it all on ONE asset when you could spend it on several? You could spend a portion on the down payment of a home, some on a rental property, and the rest on other investments like a business or stocks. Leverage and diversification of assets and income are key! [See this post: How to Invest with $1,000]

As the featured image on this post says- there’s much to be done and undone. There’s so much more bad advice that Dave Ramsey put’s out there that needs to be “undone” in the minds of many, but I’d literally have to write a book to cover it all. Dave Ramsey’s teachings are not only misleading, but the way he speaks about people and to people is really discouraging. You should be in a community where you are uplifted and empowered and where realistic examples are shared. If you’re looking to join a group of like minded people, we’d love to have you in The Key Resource facebook group community! It’s absolutely free to join. See you in the group!

LET’S CONNECT!

YouTube | Instagram | Facebook | Twitter

For collaborations please email 📧 hello {at} getthekeyresource.com